China Betting Against the U.S. Dollar

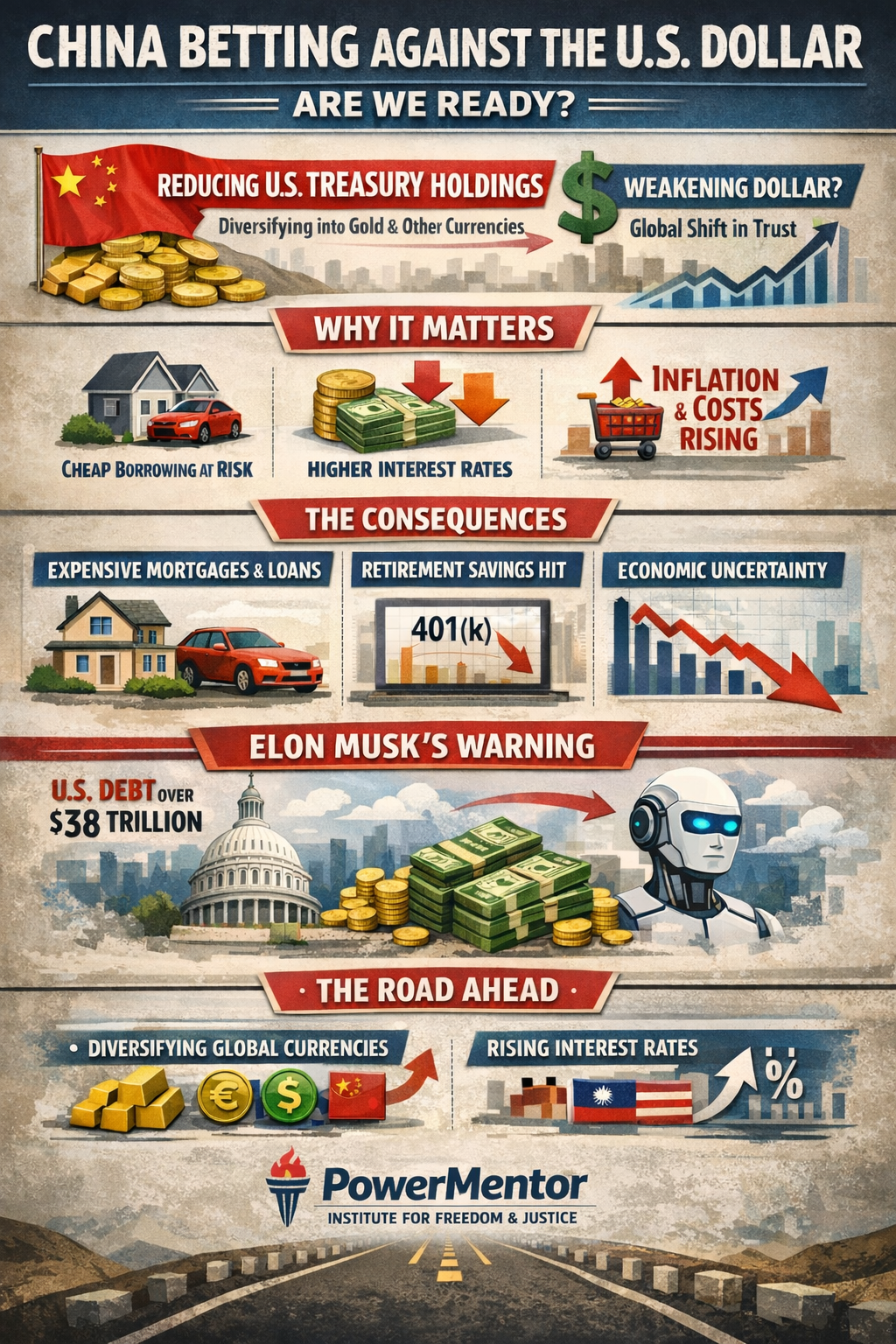

The global financial system runs on trust, and a big part of that trust has been anchored in the U.S. dollar and U.S. Treasuries (U.S. government bonds). When major economies and large banks treat Treasuries as the “default safe asset,” it keeps global money flowing smoothly and helps the United States borrow at relatively lower cost. That arrangement has supported cheaper credit, stable markets, and the dollar’s outsized role in world trade and reserves.

A quiet but meaningful shift happens when large holders—especially big institutions in places like China—start reducing concentration risk in U.S. Department of the Treasury securities. This doesn’t need to look like a dramatic sell-off to matter. Even gradual “diversify a little more” behavior can signal to other investors that they should reconsider how much of their safety and liquidity depends on one country’s debt and one currency system. Over time, that can nudge the world toward a more diversified mix of reserves—more gold, more non-dollar currencies, more regional settlement systems.

If demand for U.S. Treasuries weakens at the margin, the downstream effects can land in everyday life. The most direct channel is interest rates: to attract buyers, borrowing costs may need to rise, which can mean more expensive mortgages, auto loans, and business financing. A second channel is the exchange rate: if the dollar weakens, imports can cost more, feeding inflation and reducing purchasing power. Even without a sudden crisis, a slow erosion of confidence can translate into higher costs, slower growth, and choppier markets that impact retirement accounts and long-term savings.

The most grounded way to track this issue is to watch for persistent, multi-year patterns rather than headlines: changes in major reserve allocations, shifts in international trade settlement away from dollars, sustained moves in Treasury demand, and the trajectory of U.S. debt servicing costs relative to revenues. The core point isn’t that the dollar “collapses tomorrow,” but that incremental repositioning by big players can raise the price of borrowing and reduce strategic flexibility over time if the U.S. doesn’t pair innovation with credible fiscal discipline.